The Shortfalls of Oklahoma’s Defined Benefit Public Pension Plans

November 19, 2014

Tulsa Pension System Is Underestimating Its Debt and Investment Risk by Millions

Substantive, structural reform to the way Tulsa offers retirement benefits to its city employees is necessary in the immediate future in order to prevent these fiscal challenges from overwhelming the city budget and weighing down heavily on Tulsa taxpayers.

Adobe Acrobat document [1.3 MB]

August 13, 2014

Expectations of future policy changes, including tax increases and reduced government services, can affect the business climate and labor market within a state. Unfunded public pension liabilities represent a significant source of concern, especially given the guaranteed nature of pension benefits to retirees. Current government statistics obfuscate the underfunding of public pensions. A proper accounting of public pension liabilities shows an increased risk of tax increases and reduced government services. Unfunded public pension obligations are not the only source of such policy changes, but they remain a significant threat to the states’ fiscal health and therefore to the business climate and labor markets within the states. Due to ongoing changes in state pension programs, a slow but continuing economic recovery, and the advent of new accounting rules, this underscores the need for wide-ranging pension reform that assures proper funding of pensions well into the future.

Adobe Acrobat document [1.0 MB]

March 20, 2014

Across the country, unfunded public pension liabilities are the single largest threat to the stability and solvency of state and municipal governments. According to 2013 valuations, Oklahoma’s six active defined benefit plans, plus the Wildlife Conservation Retirement Plan, which was recently closed to new members, carry an $11.4 billion unfunded liability. They have a combined funded ratio of 66.5 percent. This unfunded liability exceeds the state-appropriated budget by 52 percent. A more accurate accounting suggests that the problem is actually more serious—Oklahoma’s public pension systems have a $43.7 billion unfunded liability. Fortunately, there is a solution that allows Oklahoma to keep its promises to current employees and retirees, protect taxpayers and communities, and ensure long-term fiscal health. The state should close its defined benefit pension systems to new members and instead institute a defined contribution (DC) alternative. A DC plan would give new employees a secure retirement.

Adobe Acrobat document [2.6 MB]

Get in Touch With Me.

Call me at 405 810-8119 with any questions or to schedule an appointment.

Greg Karnes CPA

4301 NW 63rd St, Suite 200

Oklahoma City, OK 73116-1504

Or you may use my contact form.

Competitive Fee Structure

… but if you are looking for the cheapest fees, or obsessing about your correct pronouns or global warming/white privilege B.S., or unable to make up your mind as to whether you are a man or a woman, you would be so much happier working with someone else…

… in addition, due to an extremely hectic schedule, only serious inquiries may expect a response …

New tax clients are expected to provide copies of their last 3 years of tax returns and provide permission to contact prior accountant to resolve any issues, if necessary.

Regretfully, I am unable to accept new clients who have unfiled prior-year’s tax returns, who are not current with all prior tax obligations, are involved in any marijuana-related business ventures, use marijuana or illegal drugs, have any income from gambling, invest in cryptocurrency, are experiencing extreme financial difficulties, are personal-injury attorneys, in the construction industry or are in the country illegally. Newly formed businesses are frowned upon as well.

Though not required, supporters of President Donald J. Trump, Governor Kevin Stitt, the National Rifle Association & clients who are alpha males & females, ethical, hard-working, cheerful, optimistic and NOT easily offended are generally preferred.

Absolutely NO LAZY, TREE-HUGGING, CRITICAL RACE THEORY PROMOTING, ECONOMICALLY ILLITERATE, GODLESS, RIOTING, KNEELING, CENSORING, RACIALLY & GENDER OBSESSED, DR. SEUSS BOOK-BANNING, FIREARM CONFISCATING, BIG GOVERNMENT SOCIALISTS allowed beyond the front door, however!

Due to the alleged gang activity and drug dealing at the nearby Chelsea Manor Apts. & 7-11 Convenience Store, I would personally recommend "packing some heat" while in this area (and perhaps Penn Square Mall as well). Some believe the OKC Police Dept. has become too constrained and are hesitant to confront these gangbangers and put them behind bars where they rightfully belong. "Talk on the Street" seems to be that this emanates from an extremely weak & naive Mayor who purportedly suffers from a severe case of "Low T," a weak City Manager, a new, effeminate-looking Police Chief, who refuses to enforce our nation's immigration laws & a Ward 6 Council Girl who took her Oath Of Office using a book on Marxism.

Anyone that treats black Americans differently does so because @BarackObama has been saying that they are different for the last 10 years. The reality is, they are not and should not be. https://t.co/YxuH5rHjUW pic.twitter.com/0Et5yXEMl1

— Bernard B. Kerik (@BernardKerik) April 20, 2021

Everything that Mayor David “Pajama Boy” Holt & Police Chief “Wily” Wade Gourley need to know to improve law enforcement in OKC is in this book…if only they had some courage...

Calm Guide Sheet by Greg Karnes on Scribd

When you are hunting elephants, don’t get distracted chasing rabbits.

— T. Boone Pickens (@boonepickens) March 7, 2011

... coming from someone who should know! https://t.co/H2OwzJquyg via @TMZ_Sports

— Greg Karnes (@realGregKarnes) January 3, 2019

The duration of a mass shooting always depends on the arrival of the 2nd gun.

— longhorn_92 (@jaelvoet) December 30, 2019

And Democrats want to ban you from protecting yourself. Remember that next time you vote. pic.twitter.com/7N6GBPwYig

✅ An #ArmedCitizen saved multiple lives last night in #OKC. We hope this serves as a wake-up call for @GovMaryFallin, who just two weeks ago vetoed a constitutional carry bill. Just another example of how the best way to stop a bad guy with a gun is a good guy with a gun. #2A pic.twitter.com/kPRjpiyeow

— NRA (@NRA) May 25, 2018

Need to be a long-time Sooner football fan to appreciate.

— Greg Karnes (@realGregKarnes) February 22, 2020

Video taken 2 1/2 years ago in a friend's kitchen.

Former Sooner broadcaster John "Disco" Brooks & Marcus Dupree.

Also cameo by former Sooner/Sam Bradford's dad, Kent, & former Mayor Mick Cornett. pic.twitter.com/f5VZKxuvsm

Make The University of Oklahoma Great Again!

(Let us return to the time before the “Loudmouth Communist Snowflakes” and the less than competent financial administrators arrived on campus)

At the University of Oklahoma, the researchers found there were nearly nine registered Democrats for every one Republican on the faculty, and faculty gave $2 in campaign contributions to Democrats for every $1 given to Republicanshttps://t.co/l4Pzb3b5Q9

— Greg Karnes (@realGregKarnes) February 2, 2020

Citing Black Lives Matter, photos of retired white male professors to be taken down at U. Oklahoma

— Greg Karnes (@realGregKarnes) August 26, 2020

...I keep telling people that my alma mater has become a hotbed of Marxist thinking...

https://t.co/vutEDHcNpm

Are these ridiculous demands an inevitable consequence of my alma mater staffing the University with so many card-carrying Marxists?https://t.co/9LY2o7OsBr

— Greg Karnes (@realGregKarnes) August 10, 2020

Sadly, the University of Oklahoma is becoming a hotbed of Communist snowflakes.

— Greg Karnes (@realGregKarnes) September 27, 2019

Perhaps someday we can rebuild the University back to something that the football team can be proud of! https://t.co/Y0DrXXyUjN via @OUDaily

Looks to me some government employee violated the law. pic.twitter.com/5zOuXd8aei

— Mark Sharpton (@MarkSharpton) February 23, 2020

Pledge of Allegiance removed from OU undergraduate congressional agenda.

— Greg Karnes (@realGregKarnes) September 27, 2019

Student Philip Aldridge seems to have nailed it.https://t.co/DEtZId6xmP

Former OU volleyball player sues over exclusion from team because of Conservative political views

— Greg Karnes (@realGregKarnes) June 3, 2021

...my alma mater continues its trend towards forcing Marxist & radical views on the student body...hope she takes them to the cleanershttps://t.co/VSA5B60CZD

ODELL BECKHAM JR.

NOVEMBER 23, 2014

GREATEST CATCH EVER ??

RUSSELL WESTBROOK

FEBRUARY 16, 2015

NBA ALL STAR GAME MVP

41 POINTS

3RD MOST EVER SCORED

OU SOONER - SAMAJE PERINE

NOVEMBER 22, 2014

427 RUSHING YARDS

MOST EVER BY A COLLEGE RUNNING BACK

1/ Known for basketball prowess, Wayman Tisdale's 'further legacy is his love of God'

— Greg Karnes (@realGregKarnes) April 10, 2021

...saw this story in today's paper regarding Wayman Tisdale and couldn't help but be reminded of Toby Keith's tribute song to his friend...https://t.co/4RiPYofGB7

Top 10

Taxpayer Enemies

Those Individuals Or Groups Who Seem Most Intent On Penalizing Success & Achievement & Desiring A Return To The Days Of Low Economic Growth During The Jimmy Carter/Barry Obama - "Sleepy Joe" Biden Era

(in order, as of today)

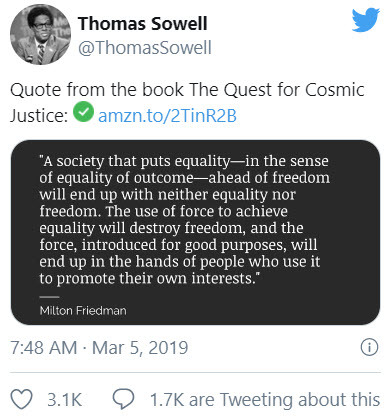

“Since this is an era when many people are concerned about ‘fairness’ and ‘social justice,’ what is your ‘fair share’ of what someone else has worked for?”

— Thomas Sowell (@ThomasSowell) January 8, 2019

The Caracas Caucus

(the Top 10 “Americans” who seem most hell-bent on destroying our jobs & economy in order to advance the cause of centralized government control over our lives and private businesses to the point where we are forced to surrender our individual liberties to the state)

— Greg Karnes (@realGregKarnes) March 29, 2021

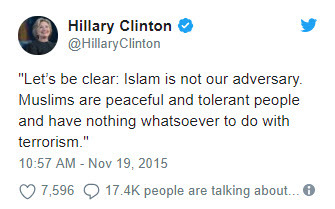

The Terrorist Caucus

Those Individuals Or Groups Who

Come Across To Me As Ambivalent Towards Islamic

Terror Activities

The "Soft On Crime"

"Hug-A-Thug" Caucus

The Top 10 Individuals Or Groups Who

Come Across To Me As Coddling The Criminal Element At The Expense Of The Public Safety Of Law-Abiding Citizens

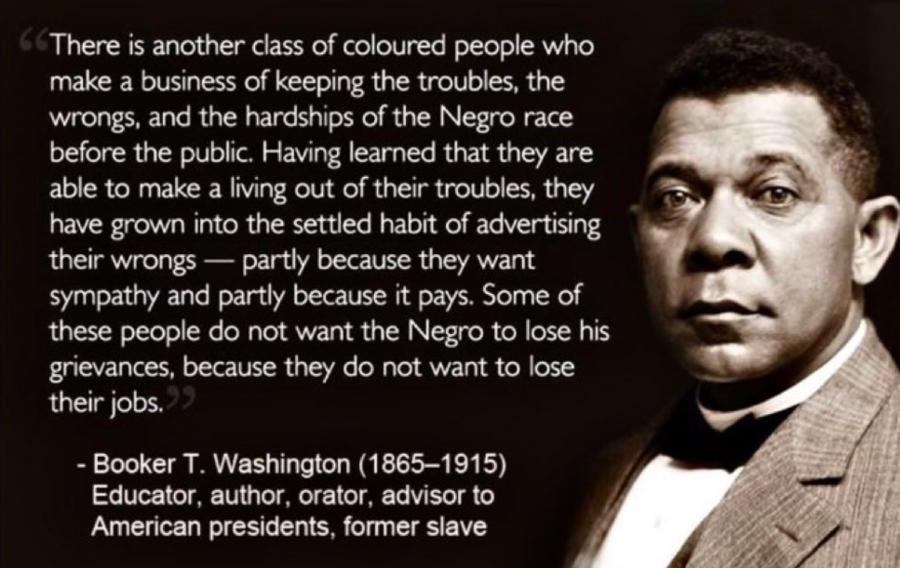

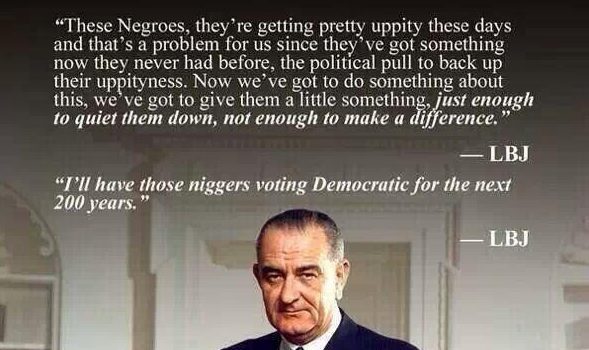

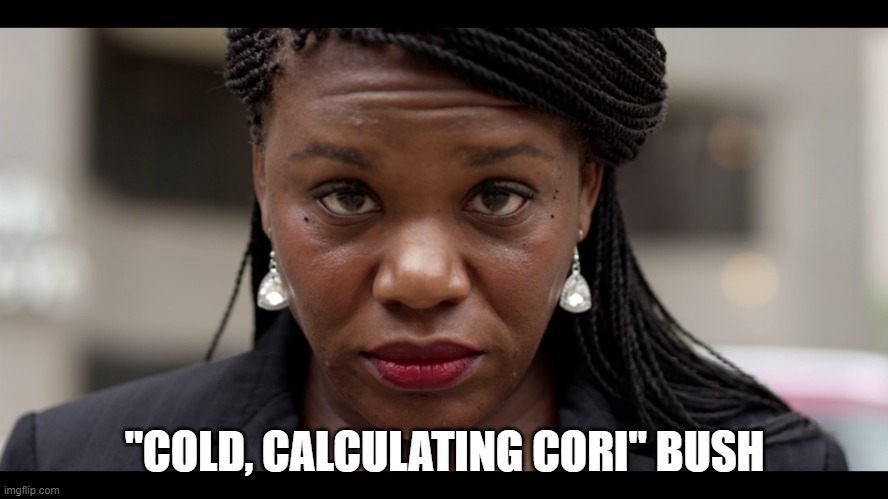

The “Ugly” Caucus

The Top 10 Individuals On The Taxpayer Payroll That Strike Me As Being Just As Unattractive On The Inside As They Are On The Outside.

LOWER TAXES

=

HIGHER GOVERNMENT REVENUE

This should be simple enough for everyone to understand. pic.twitter.com/tWsu50ewvL

— Juanita Broaddrick (@atensnut) October 21, 2021

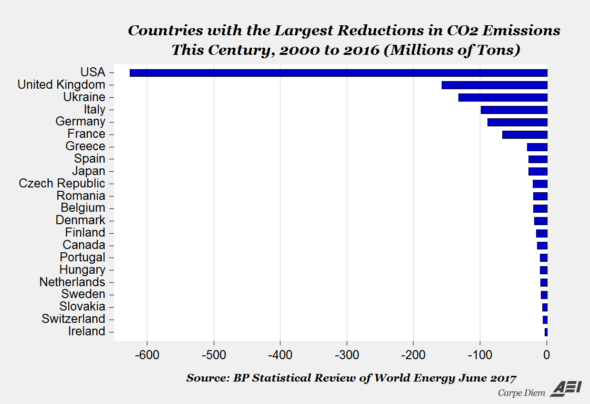

The United States leads the world in CO2 reductions

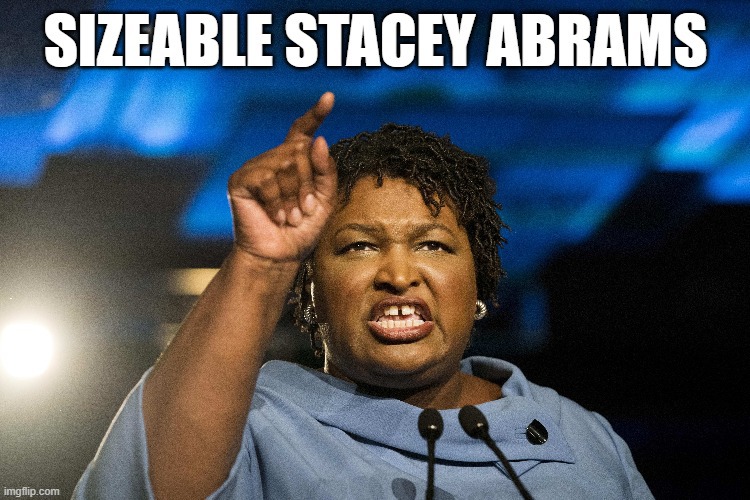

Is the individual depicted above the most ill-prepared person Oklahoma has ever had in a General Election for a U.S. Senate seat?